注釈

このページは docs/tutorials/08_cvar_optimization.ipynb から生成されました。

CVaRを使用した変分量子最適化の改善#

はじめに#

このノートブックは、Qiskit Algorithms <https://qiskit.org/ecosystem/algorithms/>`__が提供する変分量子最適化アルゴリズム内で [1] で紹介されたConditional Value at Risk (CVaR) 目的関数を使用する方法を示しています。 特に、 ``SamplingVQE` を使用して MinimumEigenOptimizer を設定する方法を示します。 考慮される最適化問題に対応する客観的価値を持つショットの特定のセットについて、信頼水準 \(\alpha \in [0, 1]\) のCVaRは、 \(\alpha\) ベストショットの平均として定義されます。 したがって、 \(\alpha = 1\) は標準の期待値に対応し、 \(\alpha=0\) は与えられたショットの最小値に対応し、 \(\alpha \in (0, 1)\) はより良いショットに焦点を合わせる間のトレードオフですが、最適化ランドスケープをスムーズにするために平均化を適用します。

参考文献#

[1] P. Barkoutsos et al., Improving Variational Quantum Optimization using CVaR, Quantum 4, 256 (2020).

[1]:

from qiskit.circuit.library import RealAmplitudes

from qiskit_algorithms.optimizers import COBYLA

from qiskit_algorithms import NumPyMinimumEigensolver, SamplingVQE

from qiskit_algorithms.utils import algorithm_globals

from qiskit.primitives import Sampler

from qiskit_optimization.converters import LinearEqualityToPenalty

from qiskit_optimization.algorithms import MinimumEigenOptimizer

from qiskit_optimization.translators import from_docplex_mp

import numpy as np

import matplotlib.pyplot as plt

from docplex.mp.model import Model

[2]:

algorithm_globals.random_seed = 123456

ポートフォリオの最適化#

以下では、 [1] で紹介したポートフォリオ最適化の問題インスタンスを定義します。

[3]:

# prepare problem instance

n = 6 # number of assets

q = 0.5 # risk factor

budget = n // 2 # budget

penalty = 2 * n # scaling of penalty term

[4]:

# instance from [1]

mu = np.array([0.7313, 0.9893, 0.2725, 0.8750, 0.7667, 0.3622])

sigma = np.array(

[

[0.7312, -0.6233, 0.4689, -0.5452, -0.0082, -0.3809],

[-0.6233, 2.4732, -0.7538, 2.4659, -0.0733, 0.8945],

[0.4689, -0.7538, 1.1543, -1.4095, 0.0007, -0.4301],

[-0.5452, 2.4659, -1.4095, 3.5067, 0.2012, 1.0922],

[-0.0082, -0.0733, 0.0007, 0.2012, 0.6231, 0.1509],

[-0.3809, 0.8945, -0.4301, 1.0922, 0.1509, 0.8992],

]

)

# or create random instance

# mu, sigma = portfolio.random_model(n, seed=123) # expected returns and covariance matrix

[5]:

# create docplex model

mdl = Model("portfolio_optimization")

x = mdl.binary_var_list(range(n), name="x")

objective = mdl.sum([mu[i] * x[i] for i in range(n)])

objective -= q * mdl.sum([sigma[i, j] * x[i] * x[j] for i in range(n) for j in range(n)])

mdl.maximize(objective)

mdl.add_constraint(mdl.sum(x[i] for i in range(n)) == budget)

# case to

qp = from_docplex_mp(mdl)

[6]:

# solve classically as reference

opt_result = MinimumEigenOptimizer(NumPyMinimumEigensolver()).solve(qp)

print(opt_result.prettyprint())

objective function value: 1.27835

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

[7]:

# we convert the problem to an unconstrained problem for further analysis,

# otherwise this would not be necessary as the MinimumEigenSolver would do this

# translation automatically

linear2penalty = LinearEqualityToPenalty(penalty=penalty)

qp = linear2penalty.convert(qp)

_, offset = qp.to_ising()

SamplingVQEを使用した最小固有オプティマイザー(Minimum Eigen Optimizer)#

[8]:

# set classical optimizer

maxiter = 100

optimizer = COBYLA(maxiter=maxiter)

# set variational ansatz

ansatz = RealAmplitudes(n, reps=1)

m = ansatz.num_parameters

# set sampler

sampler = Sampler()

# run variational optimization for different values of alpha

alphas = [1.0, 0.50, 0.25] # confidence levels to be evaluated

[9]:

# dictionaries to store optimization progress and results

objectives = {alpha: [] for alpha in alphas} # set of tested objective functions w.r.t. alpha

results = {} # results of minimum eigensolver w.r.t alpha

# callback to store intermediate results

def callback(i, params, obj, stddev, alpha):

# we translate the objective from the internal Ising representation

# to the original optimization problem

objectives[alpha].append(np.real_if_close(-(obj + offset)))

# loop over all given alpha values

for alpha in alphas:

# initialize SamplingVQE using CVaR

vqe = SamplingVQE(

sampler=sampler,

ansatz=ansatz,

optimizer=optimizer,

aggregation=alpha,

callback=lambda i, params, obj, stddev: callback(i, params, obj, stddev, alpha),

)

# initialize optimization algorithm based on CVaR-SamplingVQE

opt_alg = MinimumEigenOptimizer(vqe)

# solve problem

results[alpha] = opt_alg.solve(qp)

# print results

print("alpha = {}:".format(alpha))

print(results[alpha].prettyprint())

print()

alpha = 1.0:

objective function value: 1.2783500000000174

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

alpha = 0.5:

objective function value: 1.2783500000000174

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

alpha = 0.25:

objective function value: 1.2783500000000174

variable values: x_0=1.0, x_1=1.0, x_2=0.0, x_3=0.0, x_4=1.0, x_5=0.0

status: SUCCESS

[10]:

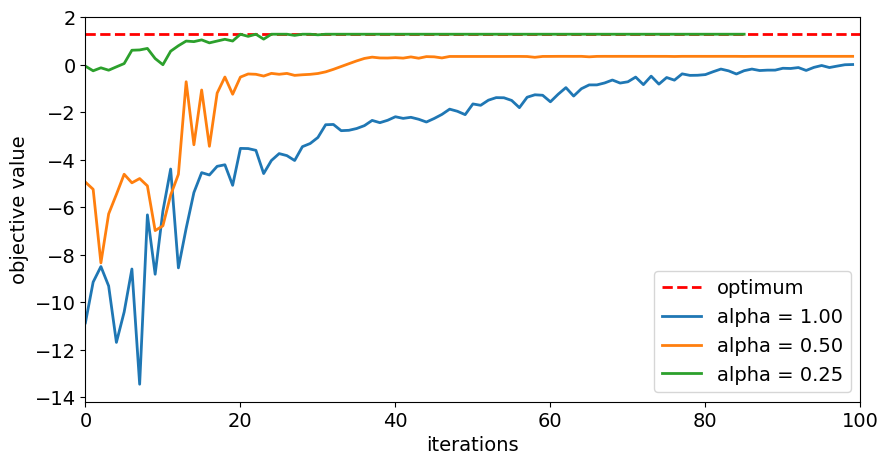

# plot resulting history of objective values

plt.figure(figsize=(10, 5))

plt.plot([0, maxiter], [opt_result.fval, opt_result.fval], "r--", linewidth=2, label="optimum")

for alpha in alphas:

plt.plot(objectives[alpha], label="alpha = %.2f" % alpha, linewidth=2)

plt.legend(loc="lower right", fontsize=14)

plt.xlim(0, maxiter)

plt.xticks(fontsize=14)

plt.xlabel("iterations", fontsize=14)

plt.yticks(fontsize=14)

plt.ylabel("objective value", fontsize=14)

plt.show()

[11]:

# evaluate and sort all objective values

objective_values = np.zeros(2**n)

for i in range(2**n):

x_bin = ("{0:0%sb}" % n).format(i)

x = [0 if x_ == "0" else 1 for x_ in reversed(x_bin)]

objective_values[i] = qp.objective.evaluate(x)

ind = np.argsort(objective_values)

# evaluate final optimal probability for each alpha

for alpha in alphas:

probabilities = np.fromiter(

results[alpha].min_eigen_solver_result.eigenstate.binary_probabilities().values(),

dtype=float,

)

print("optimal probability (alpha = %.2f): %.4f" % (alpha, probabilities[ind][-1:]))

optimal probability (alpha = 1.00): 0.0000

optimal probability (alpha = 0.50): 0.0000

optimal probability (alpha = 0.25): 0.2895

[12]:

import qiskit.tools.jupyter

%qiskit_version_table

%qiskit_copyright

Version Information

| Qiskit Software | Version |

|---|---|

qiskit-terra | 0.25.0.dev0+1d844ec |

qiskit-aer | 0.12.0 |

qiskit-ibmq-provider | 0.20.2 |

qiskit-nature | 0.7.0 |

qiskit-optimization | 0.6.0 |

| System information | |

| Python version | 3.10.11 |

| Python compiler | Clang 14.0.0 (clang-1400.0.29.202) |

| Python build | main, Apr 7 2023 07:31:31 |

| OS | Darwin |

| CPUs | 4 |

| Memory (Gb) | 16.0 |

| Thu May 18 16:56:49 2023 JST | |

This code is a part of Qiskit

© Copyright IBM 2017, 2023.

This code is licensed under the Apache License, Version 2.0. You may

obtain a copy of this license in the LICENSE.txt file in the root directory

of this source tree or at http://www.apache.org/licenses/LICENSE-2.0.

Any modifications or derivative works of this code must retain this

copyright notice, and modified files need to carry a notice indicating

that they have been altered from the originals.

[ ]: